Call options are financial contracts that give the holder the right, but not the obligation, to buy a specified underlying asset at a predetermined strike price on or before a specified expiration date. Open interest refers to the total number of outstanding contracts that have not been exercised or expired.

In the options market, open interest is a key metric that can provide valuable information about market sentiment and the level of activity in a particular contract. It can be used in combination with other indicators, such as trading volume and price movements, to gain a better understanding of market conditions.

One way that traders use open interest is to determine the level of bullish or bearish sentiment in the market. For example, if the open interest for call options on a particular stock is increasing, it may indicate that traders are becoming more bullish on the stock, as they are buying up more call options. Similarly, if the open interest for put options on a stock is increasing, it may indicate that traders are becoming more bearish on the stock.

Another way that traders use open interest is to gauge the level of liquidity and volatility in a particular contract. A high level of open interest may indicate that there is a large number of buyers and sellers active in the market, which can make it easier to enter and exit trades. This can also make the market more volatile, as there are more participants that can push prices in different directions. A low level of open interest, on the other hand, may indicate that there are fewer traders active in the market, which can make it harder to enter and exit trades and may lead to less volatility.

Open interest can also be used to track the activity of large institutional traders, such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their open interest positions can have a significant impact on the market.

In conclusion, Call options open interest is an indicator that shows the total outstanding number of call options contracts that have not been exercised or expired. It is an important metric that can provide valuable information about market sentiment, liquidity, volatility, and the activity of large institutional traders. Traders use it in combination with other indicators to gain a better understanding of market conditions and make informed trading decisions.

Put options are financial contracts that give the holder the right, but not the obligation, to sell a specified underlying asset at a predetermined strike price on or before a specified expiration date. Like call options, the open interest of put options refers to the total number of outstanding contracts that have not been exercised or expired.

Open interest is an important metric for traders and investors in the options market, as it can provide valuable information about market sentiment and the level of activity in a particular contract. It can be used in combination with other indicators, such as trading volume and price movements, to gain a better understanding of market conditions.

One way that traders use put open interest is to determine the level of bearish or bullish sentiment in the market. For example, if the open interest for put options on a particular stock is increasing, it may indicate that traders are becoming more bearish on the stock, as they are buying up more put options in anticipation of a price decline. Similarly, if the open interest for call options on a stock is increasing, it may indicate that traders are becoming more bullish on the stock.

Another way that traders use put open interest is to gauge the level of liquidity and volatility in a particular contract. A high level of put open interest may indicate that there are a large number of buyers and sellers active in the market, which can make it easier to enter and exit trades. This can also make the market more volatile, as there are more participants that can push prices in different directions. A low level of put open interest, on the other hand, may indicate that there are fewer traders active in the market, which can make it harder to enter and exit trades and may lead to less volatility.

Traders also use put open interest to track the activity of large institutional traders, such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their open interest positions can have a significant impact on the market.

In conclusion, put open interest is an indicator that shows the total outstanding number of put options contracts that have not been exercised or expired. It is an important metric that can provide valuable information about market sentiment, liquidity, volatility, and the activity of large institutional traders. Traders use it in combination with other indicators to gain a better understanding of market conditions and make informed trading decisions.

The put/call open interest ratio is a tool used by traders and investors to determine the level of bullish or bearish sentiment in the options market. The ratio is calculated by dividing the total open interest of put options by the total open interest of call options. This ratio can provide valuable information about the sentiment of market participants and the level of activity in the options market.

A put/call open interest ratio of less than 1 indicates that there is more open interest in call options than in put options, which typically means that the market is bullish. In this case, traders believe that the underlying asset’s price will rise. On the other hand, a put/call open interest ratio of more than 1 indicates that there is more open interest in put options than in call options, which typically means that the market is bearish. Traders believe that the underlying asset’s price will fall.

It’s important to note that the put/call open interest ratio alone can’t be used to predict market direction, but instead should be used in conjunction with other indicators, such as trading volume and price movements, to gain a better understanding of market conditions.

The ratio can also be used to track the activity of large institutional traders, such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their open interest positions can have a significant impact on the market.

Another use for the put/call open interest ratio is for traders who are implementing options strategies as it can be used as a measure to confirm or refute the current market assumptions. A high ratio could indicate that market participants are expecting a bearish market, while a low ratio could indicate that they are expecting a bullish market.

In conclusion, the put/call open interest ratio is a useful tool for traders and investors to gauge the level of bullish or bearish sentiment in the options market. A ratio less than 1 means that there’s more open interest in call options which is a sign of bullishness. A ratio more than 1 indicates that there’s more open interest in put options which is a sign of bearishness. It can provide valuable information about market conditions and the activity of large institutional traders when used in combination with other indicators.

Implied volatility is a measure of the expected volatility of the underlying asset’s price, as implied by the price of its options. It is a theoretical value that is derived from the price of the options using a mathematical model such as the Black-Scholes model.

Implied volatility is an important concept for options traders and investors, as it can provide valuable information about the level of risk associated with a particular option. Generally, options with higher implied volatility are considered to be more risky, as they have a greater potential for price movement in either direction. Options with lower implied volatility, on the other hand, are considered to be less risky, as they have less potential for price movement.

Traders use implied volatility in a number of ways to inform their trading decisions. Some traders use it to measure the level of risk associated with a particular option, while others use it to predict the future price movements of the underlying asset. Some traders also use it to help select options with the right level of risk for their trading strategy.

When implied volatility is high, options prices are generally higher, because they are perceived to be riskier. Conversely, when implied volatility is low, options prices are generally lower, because they are perceived to be less risky.

One of the ways to use implied volatility is through volatility smile. A volatility smile is a graphical representation of the implied volatility for options with different strike prices. It is used to indicate that implied volatility is not the same for all strikes, implying that the market participants have different views on the volatility of the underlying asset. This can be used to find the most profitable options to trade by using the options with highest implied volatility.

In conclusion, Implied volatility is a key metric for options traders and investors. It is a theoretical value that is derived from the options prices using a mathematical model, such as the Black-Scholes model. It measures the expected volatility of the underlying asset’s price. High implied volatility indicates that the option is perceived as riskier, while low implied volatility indicates that the option is perceived as less risky. Traders use implied volatility in a number of ways to inform their trading decisions, and also helps to find the most profitable options by using the options with highest implied volatility and volatility smile.

Implied volatility is a measure of the expected volatility of the underlying asset’s price, as implied by the price of its options. It is a theoretical value that is derived from the price of the options using a mathematical model such as the Black-Scholes model.

Implied volatility is an important concept for options traders and investors, as it can provide valuable information about the level of risk associated with a particular option. Generally, options with higher implied volatility are considered to be more risky, as they have a greater potential for price movement in either direction. Options with lower implied volatility, on the other hand, are considered to be less risky, as they have less potential for price movement.

Traders use implied volatility in a number of ways to inform their trading decisions. Some traders use it to measure the level of risk associated with a particular option, while others use it to predict the future price movements of the underlying asset. Some traders also use it to help select options with the right level of risk for their trading strategy.

When implied volatility is high, options prices are generally higher, because they are perceived to be riskier. Conversely, when implied volatility is low, options prices are generally lower, because they are perceived to be less risky.

One of the ways to use implied volatility is through volatility smile. A volatility smile is a graphical representation of the implied volatility for options with different strike prices. It is used to indicate that implied volatility is not the same for all strikes, implying that the market participants have different views on the volatility of the underlying asset. This can be used to find the most profitable options to trade by using the options with highest implied volatility.

In conclusion, Implied volatility is a key metric for options traders and investors. It is a theoretical value that is derived from the options prices using a mathematical model, such as the Black-Scholes model. It measures the expected volatility of the underlying asset’s price. High implied volatility indicates that the option is perceived as riskier, while low implied volatility indicates that the option is perceived as less risky. Traders use implied volatility in a number of ways to inform their trading decisions, and also helps to find the most profitable options by using the options with highest implied volatility and volatility smile.

Historical volatility is a measure of the volatility of the underlying asset’s price, as observed over a certain period of time in the past. It is calculated by analyzing the past price movements of the underlying asset and measuring how much the price has fluctuated over a certain period. It provides a view of how much volatility has existed in the past and can be used to compare the volatility of different securities or to see if the volatility of a particular security has been increasing or decreasing over time.

Historical volatility is an important concept for options traders and investors, as it can provide valuable information about the level of risk associated with a particular option. Generally, options on underlying assets with higher historical volatility are considered to be more risky, as they have a greater potential for price movement in either direction. Options on underlying assets with lower historical volatility, on the other hand, are considered to be less risky, as they have less potential for price movement.

Traders use historical volatility in a number of ways to inform their trading decisions. Some traders use it to measure the level of risk associated with a particular option, while others use it to predict the future price movements of the underlying asset. Some traders also use it to help select options with the right level of risk for their trading strategy.

One of the common ways to use historical volatility is through volatility measures. such as standard deviation or average true range. These measures provide a quantification of the volatility of a security over a certain period.

Another use of historical volatility is in options pricing models, such as the Black-Scholes model, where it is used as an input to estimate the implied volatility of the underlying asset. The implied volatility can be then compared to the historical volatility to determine if the options are overvalued or undervalued.

In conclusion, historical volatility is a key metric for options traders and investors. It is a measure of the volatility of the underlying asset’s price as observed over a certain period of time in the past. It provides a view of how much volatility has existed in the past and can be used to compare the volatility of different securities or to see if the volatility of a particular security has been increasing or decreasing over time. Traders use historical volatility in a number of ways to inform their trading decisions, such as by using volatility measures, or by comparing it with implied volatility.

Implied volatility is a measure of the expected volatility of the underlying asset’s price, as implied by the price of its options. It is a theoretical value that is derived from the price of the options using a mathematical model such as the Black-Scholes model.

Implied volatility is an important concept for options traders and investors, as it can provide valuable information about the level of risk associated with a particular option. Generally, options with higher implied volatility are considered to be more risky, as they have a greater potential for price movement in either direction. Options with lower implied volatility, on the other hand, are considered to be less risky, as they have less potential for price movement.

Traders use implied volatility in a number of ways to inform their trading decisions. Some traders use it to measure the level of risk associated with a particular option, while others use it to predict the future price movements of the underlying asset. Some traders also use it to help select options with the right level of risk for their trading strategy.

When implied volatility is high, options prices are generally higher, because they are perceived to be riskier. Conversely, when implied volatility is low, options prices are generally lower, because they are perceived to be less risky.

One of the ways to use implied volatility is through volatility smile. A volatility smile is a graphical representation of the implied volatility for options with different strike prices. It is used to indicate that implied volatility is not the same for all strikes, implying that the market participants have different views on the volatility of the underlying asset. This can be used to find the most profitable options to trade by using the options with highest implied volatility.

In conclusion, Implied volatility is a key metric for options traders and investors. It is a theoretical value that is derived from the options prices using a mathematical model, such as the Black-Scholes model. It measures the expected volatility of the underlying asset’s price. High implied volatility indicates that the option is perceived as riskier, while low implied volatility indicates that the option is perceived as less risky. Traders use implied volatility in a number of ways to inform their trading decisions, and also helps to find the most profitable options by using the options with highest implied volatility and volatility smile.

Historical volatility is a measure of the volatility of the underlying asset’s price, as observed over a certain period of time in the past. It is calculated by analyzing the past price movements of the underlying asset and measuring how much the price has fluctuated over a certain period. It provides a view of how much volatility has existed in the past and can be used to compare the volatility of different securities or to see if the volatility of a particular security has been increasing or decreasing over time.

Historical volatility is an important concept for options traders and investors, as it can provide valuable information about the level of risk associated with a particular option. Generally, options on underlying assets with higher historical volatility are considered to be more risky, as they have a greater potential for price movement in either direction. Options on underlying assets with lower historical volatility, on the other hand, are considered to be less risky, as they have less potential for price movement.

Traders use historical volatility in a number of ways to inform their trading decisions. Some traders use it to measure the level of risk associated with a particular option, while others use it to predict the future price movements of the underlying asset. Some traders also use it to help select options with the right level of risk for their trading strategy.

One of the common ways to use historical volatility is through volatility measures. such as standard deviation or average true range. These measures provide a quantification of the volatility of a security over a certain period.

Another use of historical volatility is in options pricing models, such as the Black-Scholes model, where it is used as an input to estimate the implied volatility of the underlying asset. The implied volatility can be then compared to the historical volatility to determine if the options are overvalued or undervalued.

In conclusion, historical volatility is a key metric for options traders and investors. It is a measure of the volatility of the underlying asset’s price as observed over a certain period of time in the past. It provides a view of how much volatility has existed in the past and can be used to compare the volatility of different securities or to see if the volatility of a particular security has been increasing or decreasing over time. Traders use historical volatility in a number of ways to inform their trading decisions, such as by using volatility measures, or by comparing it with implied volatility.

Implied volatility is a measure of the expected volatility of the underlying asset’s price, as implied by the price of its options. It is a theoretical value that is derived from the price of the options using a mathematical model such as the Black-Scholes model.

Implied volatility is an important concept for options traders and investors, as it can provide valuable information about the level of risk associated with a particular option. Generally, options with higher implied volatility are considered to be more risky, as they have a greater potential for price movement in either direction. Options with lower implied volatility, on the other hand, are considered to be less risky, as they have less potential for price movement.

Traders use implied volatility in a number of ways to inform their trading decisions. Some traders use it to measure the level of risk associated with a particular option, while others use it to predict the future price movements of the underlying asset. Some traders also use it to help select options with the right level of risk for their trading strategy.

When implied volatility is high, options prices are generally higher, because they are perceived to be riskier. Conversely, when implied volatility is low, options prices are generally lower, because they are perceived to be less risky.

One of the ways to use implied volatility is through volatility smile. A volatility smile is a graphical representation of the implied volatility for options with different strike prices. It is used to indicate that implied volatility is not the same for all strikes, implying that the market participants have different views on the volatility of the underlying asset. This can be used to find the most profitable options to trade by using the options with highest implied volatility.

In conclusion, Implied volatility is a key metric for options traders and investors. It is a theoretical value that is derived from the options prices using a mathematical model, such as the Black-Scholes model. It measures the expected volatility of the underlying asset’s price. High implied volatility indicates that the option is perceived as riskier, while low implied volatility indicates that the option is perceived as less risky. Traders use implied volatility in a number of ways to inform their trading decisions, and also helps to find the most profitable options by using the options with highest implied volatility and volatility smile.

Total Options Volume for all option contracts during the day

Options trading volume refers to the total number of options contracts that have been traded on a particular underlying asset during a specific period of time. It is an important metric for options traders and investors, as it can provide valuable information about the level of activity in the options market and the level of interest in a particular option or underlying asset.

Traders use options trading volume in a number of ways to inform their trading decisions. One way is by using it to gauge the level of liquidity in the market for a particular option. A high level of options trading volume for a particular option may indicate that there are a large number of buyers and sellers active in the market, which can make it easier to enter and exit trades. A low level of options trading volume, on the other hand, may indicate that there are fewer traders active in the market, which can make it harder to enter and exit trades.

Another way traders use options trading volume is by monitoring large institutional traders such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their trading volume can have a significant impact on the market. Traders can track these large positions and can use them to predict the direction of the market

Traders also use options volume to confirm trends or signals that may be present in other technical indicators. An increase in volume can confirm the trend or signal and may indicate the option is likely to continue in the direction that has been signaled.

Options trading volume is also used to make comparisons between different options and underlying assets. Traders can use this information to identify options and underlying assets that are attracting the most trading volume, which can indicate increased investor interest.

In conclusion, options trading volume is an important metric for options traders and investors as it provides valuable information about the level of activity in the options market, the level of interest in a particular option or underlying asset and the large institutional traders positions. Traders use options trading volume in a number of ways to inform their trading decisions, such as by gauging the level of liquidity in the market, monitoring large institutional traders, and making comparisons between different options and underlying assets. It can also be used to confirm trends or signals from other technical indicators.

Percent Change between that day volume and the average of the previous 5 days

Options trading volume refers to the total number of options contracts that have been traded on a particular underlying asset during a specific period of time. It is an important metric for options traders and investors, as it can provide valuable information about the level of activity in the options market and the level of interest in a particular option or underlying asset.

Traders use options trading volume in a number of ways to inform their trading decisions. One way is by using it to gauge the level of liquidity in the market for a particular option. A high level of options trading volume for a particular option may indicate that there are a large number of buyers and sellers active in the market, which can make it easier to enter and exit trades. A low level of options trading volume, on the other hand, may indicate that there are fewer traders active in the market, which can make it harder to enter and exit trades.

Another way traders use options trading volume is by monitoring large institutional traders such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their trading volume can have a significant impact on the market. Traders can track these large positions and can use them to predict the direction of the market

Traders also use options volume to confirm trends or signals that may be present in other technical indicators. An increase in volume can confirm the trend or signal and may indicate the option is likely to continue in the direction that has been signaled.

Options trading volume is also used to make comparisons between different options and underlying assets. Traders can use this information to identify options and underlying assets that are attracting the most trading volume, which can indicate increased investor interest.

In conclusion, options trading volume is an important metric for options traders and investors as it provides valuable information about the level of activity in the options market, the level of interest in a particular option or underlying asset and the large institutional traders positions. Traders use options trading volume in a number of ways to inform their trading decisions, such as by gauging the level of liquidity in the market, monitoring large institutional traders, and making comparisons between different options and underlying assets. It can also be used to confirm trends or signals from other technical indicators.

Percent Change between that day volume and the average of the previous 30 days

Options volume

Options trading volume refers to the total number of options contracts that have been traded on a particular underlying asset during a specific period of time. It is an important metric for options traders and investors, as it can provide valuable information about the level of activity in the options market and the level of interest in a particular option or underlying asset.

Traders use options trading volume in a number of ways to inform their trading decisions. One way is by using it to gauge the level of liquidity in the market for a particular option. A high level of options trading volume for a particular option may indicate that there are a large number of buyers and sellers active in the market, which can make it easier to enter and exit trades. A low level of options trading volume, on the other hand, may indicate that there are fewer traders active in the market, which can make it harder to enter and exit trades.

Another way traders use options trading volume is by monitoring large institutional traders such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their trading volume can have a significant impact on the market. Traders can track these large positions and can use them to predict the direction of the market

Traders also use options volume to confirm trends or signals that may be present in other technical indicators. An increase in volume can confirm the trend or signal and may indicate the option is likely to continue in the direction that has been signaled.

Options trading volume is also used to make comparisons between different options and underlying assets. Traders can use this information to identify options and underlying assets that are attracting the most trading volume, which can indicate increased investor interest.

In conclusion, options trading volume is an important metric for options traders and investors as it provides valuable information about the level of activity in the options market, the level of interest in a particular option or underlying asset and the large institutional traders positions. Traders use options trading volume in a number of ways to inform their trading decisions, such as by gauging the level of liquidity in the market, monitoring large institutional traders, and making comparisons between different options and underlying assets. It can also be used to confirm trends or signals from other technical indicators.

Total Call Volume ( for all contracts ) in that day

Options call volume refers to the total number of call options contracts that have been traded on a particular underlying asset during a specific period of time. It is a metric used to gauge the level of bullish sentiment in the market for a particular underlying asset and to track the level of activity in the call options market.

Call options give the holder the right, but not the obligation, to buy a specified underlying asset at a predetermined strike price on or before a specified expiration date. When investors and traders buy call options, they are expressing a bullish sentiment on the underlying asset, as they believe the asset’s price will rise in the future. Therefore, monitoring the call options volume can provide valuable information about market sentiment and the level of interest in a particular underlying asset.

Call options volume can be used in combination with other indicators, such as trading volume and price movements, to gain a better understanding of market conditions. A high volume of call options trading for a particular underlying asset may indicate that there is a large number of buyers who are bullish on the asset, which can make it more likely that the asset’s price will rise. Conversely, a low volume of call options trading for a particular underlying asset may indicate that there is less interest in the asset, which can make it less likely that the asset’s price will rise.

Traders also use call options volume to track the activity of large institutional traders such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their call options trading volume can have a significant impact on the market. They can track these large positions and use them to predict the direction of the market.

In conclusion, Options call volume is an important metric used by traders and investors to gauge the level of bullish sentiment in the market for a particular underlying asset and to track the level of activity in the call options market. A high volume of call options trading for a particular underlying asset may indicate that there is a large number of buyers who are bullish on the asset, and conversely, a low volume of call options trading for a particular underlying asset may indicate that there is less interest in the asset. It can also be used in combination with other indicators, such as trading volume and price movements, to gain a better understanding of market conditions and also track the activity of large institutional traders.

Total Put Volume ( for all contracts ) in that day

Put options volume refers to the total number of put options contracts that have been traded on a particular underlying asset during a specific period of time. It is a metric used to gauge the level of bearish sentiment in the market for a particular underlying asset and to track the level of activity in the put options market.

Put options give the holder the right, but not the obligation, to sell a specified underlying asset at a predetermined strike price on or before a specified expiration date. When investors and traders buy put options, they are expressing a bearish sentiment on the underlying asset, as they believe the asset’s price will fall in the future. Therefore, monitoring the put options volume can provide valuable information about market sentiment and the level of interest in a particular underlying asset.

Put options volume can be used in combination with other indicators, such as trading volume and price movements, to gain a better understanding of market conditions. A high volume of put options trading for a particular underlying asset may indicate that there is a large number of buyers who are bearish on the asset, which can make it more likely that the asset’s price will fall. Conversely, a low volume of put options trading for a particular underlying asset may indicate that there is less interest in the asset, which can make it less likely that the asset’s price will fall.

Traders also use put options volume to track the activity of large institutional traders such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their put options trading volume can have a significant impact on the market. They can track these large positions and use them to predict the direction of the market.

In conclusion, Put options volume is an important metric used by traders and investors to gauge the level of bearish sentiment in the market for a particular underlying asset and to track the level of activity in the put options market. A high volume of put options trading for a particular underlying asset may indicate that there is a large number of buyers who are bearish on the asset, and conversely, a low volume of put options trading for a particular underlying asset may indicate that there is less interest in the asset. It can also be used in combination with other indicators, such as trading volume and price movements, to gain a better understanding of market conditions and also track the activity of large institutional traders.

the total put/call volume ratio for all option contracts ( across all expiration dates) traded during the current session

The put/call volume ratio is a tool used by traders and investors to determine the level of bullish or bearish sentiment in the options market. It is calculated by dividing the total volume of put options contracts by the total volume of call options contracts over a specific period of time. This ratio can provide valuable information about the sentiment of market participants and the level of activity in the options market.

A put/call volume ratio of less than 1 indicates that there is more trading volume in call options than in put options, which typically means that the market is bullish. In this case, traders believe that the underlying asset’s price will rise. On the other hand, a put/call volume ratio of more than 1 indicates that there is more trading volume in put options than in call options, which typically means that the market is bearish. Traders believe that the underlying asset’s price will fall.

It’s important to note that the put/call volume ratio alone can’t be used to predict market direction, but instead should be used in conjunction with other indicators, such as trading volume, price movements, and open interest ratio, to gain a better understanding of market conditions.

The ratio can also be used to track the activity of large institutional traders, such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their trading volume can have a significant impact on the market. By monitoring the put/call volume ratio, traders can get an insight into how institutional traders are positioning themselves in the market, which can provide valuable information for trading decisions.

Another use for the put/call volume ratio is for traders who are implementing options strategies. It can be used as a measure to confirm or refute the current market assumptions, A high ratio could indicate that market participants are expecting a bearish market, while a low ratio could indicate that they are expecting a bullish market.

In conclusion, the put/call volume ratio is a useful tool for traders and investors to gauge the level of bullish or bearish sentiment in the options market. A ratio less than 1 means that there’s more trading volume in call options which is a sign of bullishness. A ratio more than 1 indicates that there’s more trading volume in put options which is a sign of bearishness. It can provide valuable information about market conditions and the activity of large institutional traders when used in combination with other indicators.

the ATM average implied volatility relativeto the highest and lowest values over the past 1-year . If IV rank is 100% the means the IV is at its highest level over the past 1-year

Implied volatility rank (IV rank) is a measure used by options traders to compare the volatility of different options contracts or underlying assets. It is calculated by taking the implied volatility of an option or underlying asset and comparing it to the historical volatility of the same option or underlying asset over a specific period of time. The resulting number is then expressed as a percentile, with a value of 100 indicating the highest volatility and a value of 0 indicating the lowest volatility.

IV rank is a useful tool for options traders because it allows them to quickly and easily compare the volatility of different options contracts or underlying assets. It also helps traders identify options contracts or underlying assets that are currently experiencing higher or lower volatility than what is typical for that security, as well as those that may be relatively undervalued or overvalued.

For example, if an option has an IV rank of 75, it means that the current implied volatility of that option is higher than 75% of the historical implied volatility for that option over a certain period. So, if a trader is looking for options that are experiencing higher than usual volatility, they can look for options with a high IV rank. Conversely, if a trader is looking for options that are experiencing lower than usual volatility, they can look for options with a low IV rank.

Traders use IV rank in several ways, such as by comparing it with historical volatility, by using it as an input in options pricing models and using it to predict future price movements. It can also be used in combination with other indicators, such as trading volume and open interest, to gain a better understanding of market conditions.

In conclusion, Implied volatility rank (IV rank) is a measure used by options traders to compare the volatility of different options contracts or underlying assets. It is expressed as a percentile, with a value of 100 indicating the highest volatility and a value of 0 indicating the lowest volatility. IV rank is a useful tool for options traders because it allows them to quickly and easily compare the volatility of different options contracts or underlying assets, and it also helps traders identify options contracts or underlying assets that are currently experiencing higher or lower volatility than what is typical for that security. Traders use IV rank in several ways, such as by comparing it with historical volatility, by using it as an input in options pricing models and using it to predict future price.

% difference between the current volume and the 20-day average volume

Volume change refers to the difference in trading volume of a specific security or underlying asset over a certain period of time. It can be a useful indicator for traders and investors as it can provide insight into the level of buying and selling activity in the market and the level of interest in a particular security or underlying asset.

Traders often use volume change as a confirming indicator to support trends or signals that may be present in other technical indicators. For example, if a stock’s price is rising and the volume is also increasing, this can indicate that there is strong buying interest and that the upward trend in price is likely to continue. On the other hand, if a stock’s price is falling and the volume is decreasing, this can indicate that there is weak selling interest and that the downward trend in price is likely to continue.

Additionally, large changes in trading volume can also indicate potential market turning points. High trading volume can be an indication of a large number of buyers or sellers entering the market, which can cause prices to rapidly change direction. For example, if a stock is in an uptrend and suddenly there is a large increase in volume and the stock starts falling sharply, it is a sign of panic selling, which can indicate that the uptrend is over and that the stock is likely to continue falling.

Volume change can also be used to track the activity of large institutional traders such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their trading volume can have a significant impact on the market. By monitoring the volume change of a price, traders can get an insight into how institutional traders are positioning themselves in the market, which can provide valuable information for trading decisions.

In conclusion, volume change refers to the difference in trading volume of a specific security or underlying asset over a certain period of time and can provide insight into the level of buying and selling activity in the market and the level of interest in a particular security or underlying asset. Traders often use volume change as a confirming indicator to support trends or signals that may be present in other technical indicators and as an indication of potential market turning points or changes in large institutional traders activity. Volume change can be a useful indicator for traders and investors to monitor and analyze when making investment

the numbers of shares or contracts traded for the previous day.

Volume change refers to the difference in trading volume of a specific security or underlying asset over a certain period of time. It can be a useful indicator for traders and investors as it can provide insight into the level of buying and selling activity in the market and the level of interest in a particular security or underlying asset.

Traders often use volume change as a confirming indicator to support trends or signals that may be present in other technical indicators. For example, if a stock’s price is rising and the volume is also increasing, this can indicate that there is strong buying interest and that the upward trend in price is likely to continue. On the other hand, if a stock’s price is falling and the volume is decreasing, this can indicate that there is weak selling interest and that the downward trend in price is likely to continue.

Additionally, large changes in trading volume can also indicate potential market turning points. High trading volume can be an indication of a large number of buyers or sellers entering the market, which can cause prices to rapidly change direction. For example, if a stock is in an uptrend and suddenly there is a large increase in volume and the stock starts falling sharply, it is a sign of panic selling, which can indicate that the uptrend is over and that the stock is likely to continue falling.

Volume change can also be used to track the activity of large institutional traders such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their trading volume can have a significant impact on the market. By monitoring the volume change of a price, traders can get an insight into how institutional traders are positioning themselves in the market, which can provide valuable information for trading decisions.

In conclusion, volume change refers to the difference in trading volume of a specific security or underlying asset over a certain period of time and can provide insight into the level of buying and selling activity in the market and the level of interest in a particular security or underlying asset. Traders often use volume change as a confirming indicator to support trends or signals that may be present in other technical indicators and as an indication of potential market turning points or changes in large institutional traders activity. Volume change can be a useful indicator for traders and investors to monitor and analyze when making investment

the average number of shares/contracts traded over the last 1 month

The 1 month volume average indicator, also known as the 30-day average volume, is a technical indicator that is used to measure the average daily trading volume of a stock or other financial instrument over the past 30 days. It is used to determine the level of interest in a particular stock or underlying asset and to gauge the level of liquidity in the market.

The indicator is calculated by taking the total trading volume of a stock or underlying asset over the past 30 days and dividing it by 30. This provides a snapshot of the average daily trading volume for the past month, which can be used to compare the current volume to the historical average.

Traders and investors often use the 1 month volume average indicator to determine whether a stock is experiencing unusually high or low trading volume. A stock that is trading above its 30-day average volume may indicate that there is increased interest in the stock and that it may be experiencing a short-term price trend. Conversely, a stock that is trading below its 30-day average volume may indicate that there is less interest in the stock and that it may be experiencing a short-term price trend.

Additionally, the 1 month volume average indicator can also be used in combination with other technical indicators to gain a better understanding of market conditions. For example, if a stock’s price is rising and the 30-day average volume is also increasing, this can indicate that there is strong buying interest and that the upward trend in price is likely to continue. On the other hand, if a stock’s price is falling and the 30-day average volume is decreasing, this can indicate that there is weak selling interest and that the downward trend in price is likely to continue.

It’s important to note that the 1 month volume average indicator is a lagging indicator, meaning that it is based on past data and may not provide insight into future price movements. Traders and investors should use this indicator in combination with other technical and fundamental analysis tools in order to make informed investment decisions.

In conclusion, the 1 month volume average indicator, also known as the 30-day average volume, is a technical indicator

Open interest in options trading refers to the total number of options contracts that have been traded on a particular underlying asset but have not yet been closed or exercised. It is a measure of the level of activity in the options market for a particular underlying asset and can provide valuable information about market sentiment and the level of interest in that asset.

Open interest is different from trading volume, which measures the number of options contracts that have been traded on a particular underlying asset during a specific period of time. While trading volume can fluctuate from day to day, open interest reflects the total number of outstanding options contracts at any given time.

Open interest can be used in combination with other indicators, such as trading volume and price movements, to gain a better understanding of market conditions. A high open interest for a particular underlying asset may indicate that there is a large number of traders who are interested in that asset, which can make it more likely that the asset’s price will be affected by the activity in the options market.

Traders also use open interest to track the activity of large institutional traders such as hedge funds and investment banks. These traders often trade in large sizes, and changes in their open interest can have a significant impact on the market. By monitoring open interest, traders can get an insight into how institutional traders are positioning themselves in the market, which can provide valuable information for trading decisions.

Open interest can be used in several ways, such as by comparing it with trading volume, by using it as an input in options pricing models, and using it to identify trading patterns. It can also be used to confirm or refute the current market assumptions, for instance, an increase in open interest on a particular strike price of an option means that there is a high interest on that strike.

In conclusion, open interest in options trading refers to the total number of options contracts that have been traded on a particular underlying asset but have not yet been closed or exercised. It is a measure of the level of activity in the options market for a particular underlying asset and can provide valuable information about market sentiment and the level of interest in that asset. Open interest can be used in combination with other indicators, such as trading volume and price movements, to gain a better understanding

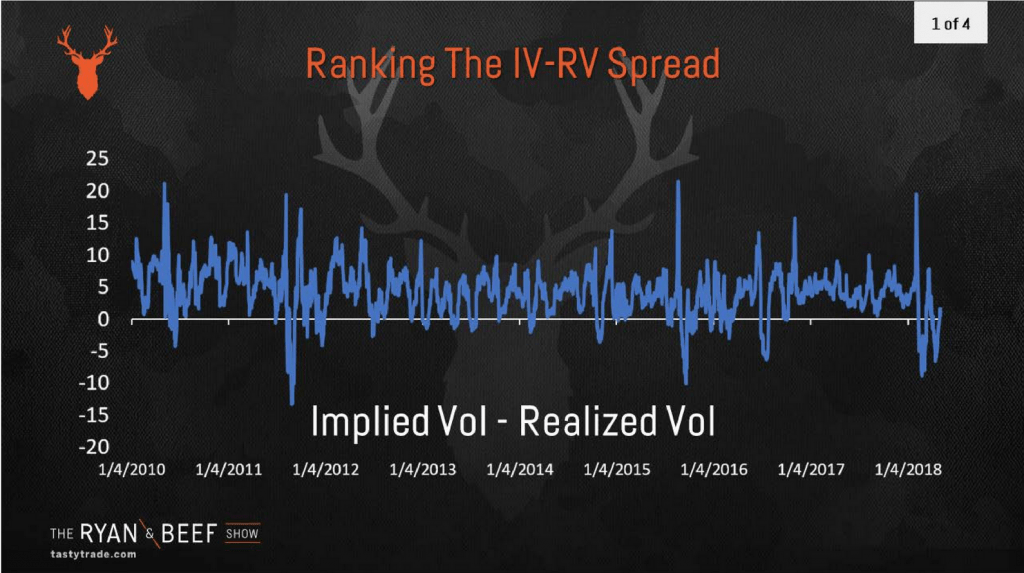

NOTE IN OUT CASE THE RATIO IS INVERSE AT THIS DESCRIPTION WE HAVE REALIZED VOLATILITY/ IMPLIED

With equity markets currently in melt-up mode and the VIX dragging near historical lows, there haven’t been a myriad of great opportunities to sell options premium.

However, while the VIX may not be flashing “sell” when it comes to short volatility, options traders have the ability to filter for potential opportunities using another tactic—namely, the spread that exists between implied volatility and realized volatility (aka actual volatility).

As most traders already know, implied volatility represents the current market price for volatility based on the market’s expectations for future movement in a given underlying. This value is “implied” by the dollar and cent value of options trading in the marketplace.

Realized volatility, on the other hand, is the actual movement that occurs in a given underlying over a defined historical period of time. Volatility traders obviously care not only about what is expected to occur, but also about what actually transpired.

For this reason, options traders often leverage the spread that exists between implied volatility (IV) and realized volatility (RV) to better gauge the relative attractiveness of a given trading opportunity.

A positive IV-RV spread indicates that implied volatility is higher than realized volatility, while a negative spread indicates the reverse. As one can see in the graphic below, historical data in SPY clearly illustrates that the bias in the IV-RV spread has been consistently positive. It’s this reality that underpins the value proposition of the short premium approach in the options marketplace:

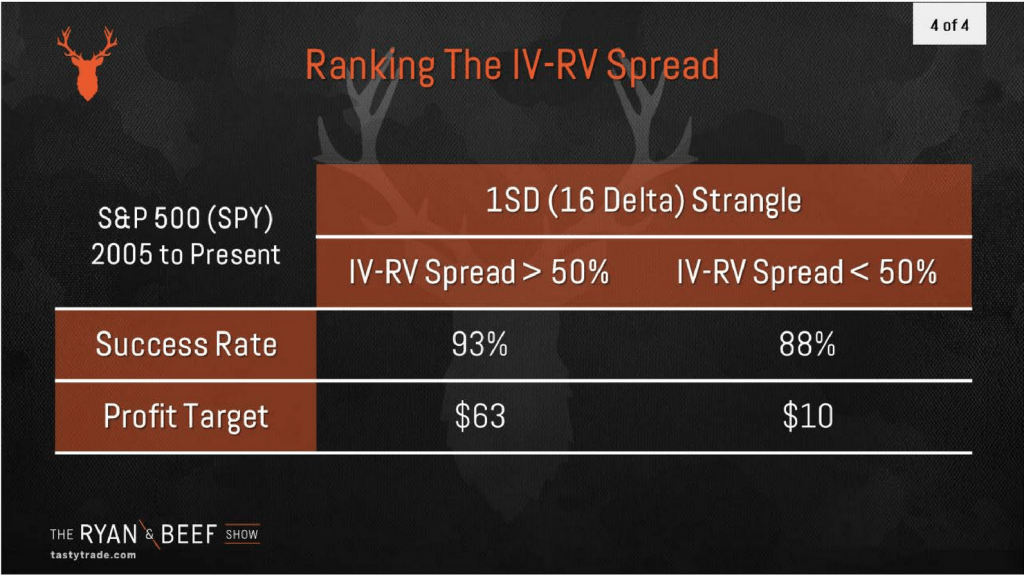

While the above is great information to be aware of, previous research conducted by the tastytrade financial network takes the practical application of the IV-RV spread one step further.

Using a series of backtests, market researchers at tastytrade looked at historical data in SPY to ascertain the performance of short strangles deployed in SPY across a range of different widths in the IV-RV spread.

As one might suspect, the findings from this research revealed that short premium approaches tend to outperform when the spread between IV and RV are at the wider end of the range, as illustrated below:

Per the findings above, short strangles in SPY have performed more efficiently (higher win rates and higher profit targets) when deployed according to a trading approach that capitalizes on wider widths in the spread between implied volatility and realized volatility.

Due to the importance of these findings, traders are encouraged to review the complete episode of Ryan & Beeffocusing on the historical spread between IV and RV when scheduling allows.

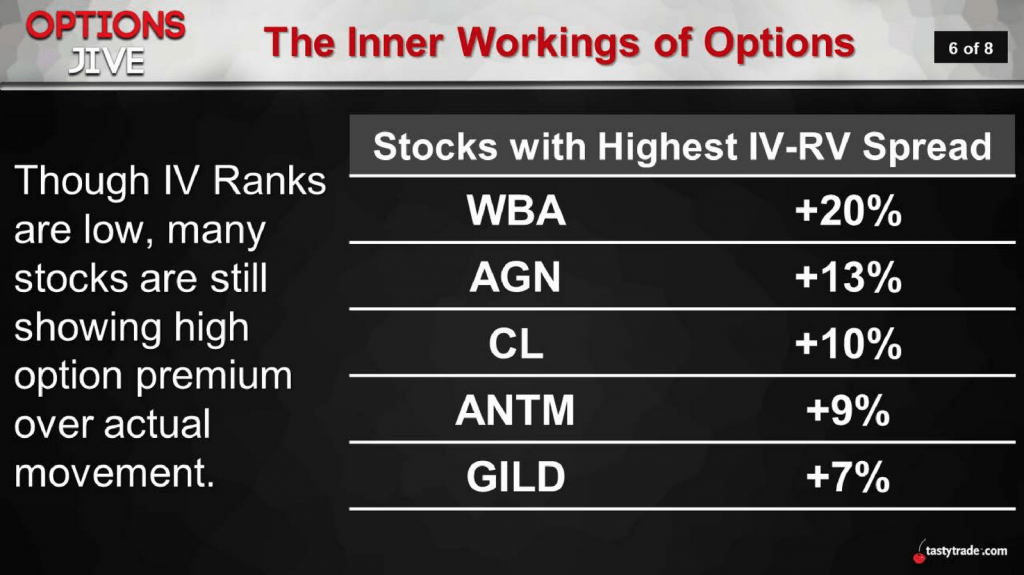

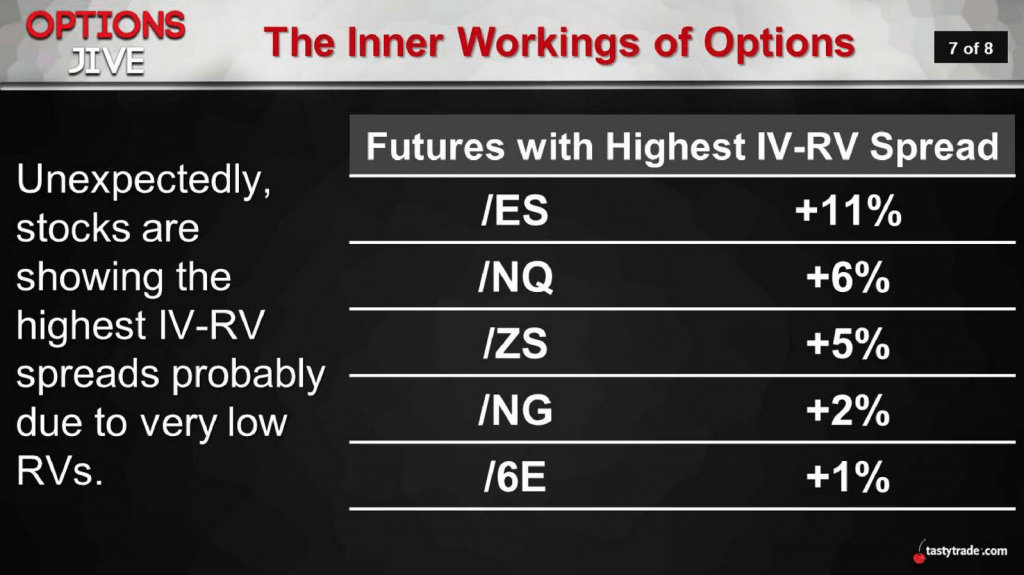

As a complement to that information, traders may want to watch a new installment of Options Jiveon the tastytrade network that focuses on current potential opportunities in both equities and futures options where the spread between IV and RV is currently the widest.

While the current low volatility environment may not compel traders to take a high degree of short volatility risk, the aforementioned approach leveraging the IV-RV spread can also be utilized in high volatility trading environments to provide additional insight on potential opportunities.

Margin of safety is a principle used by investors to reduce the risk of losing money when investing in stocks, bonds, or other securities. The margin of safety is the difference between the intrinsic value of an asset and its market price, and it is used as a measure of how undervalued or overvalued an asset is.

The idea behind margin of safety is that it allows investors to buy an asset at a price that is below its intrinsic value, providing a cushion against future market downturns. By purchasing an asset at a significant discount to its intrinsic value, investors are able to limit their potential losses and increase their chances of earning a profitable return.

One famous investor who heavily used the principle of margin of safety was Benjamin Graham, who is considered the father of value investing. He proposed that investors should only buy stocks when they are available at a discount of at least 50% to their intrinsic value to ensure they have an adequate margin of safety.

One way to estimate intrinsic value is by using a company’s financial metrics, such as price-to-earnings (P/E) ratio, price-to-book (P/B) ratio, and dividends per share, and compare them to historical averages and industry averages.

Another way to estimate intrinsic value is through the use of discounted cash flow (DCF) models. DCF models take into account a company’s projected cash flows, growth rate, and discount rate to estimate its intrinsic value.

It’s important to note that the intrinsic value is often difficult to estimate, and different methods and calculations can lead to different results. Additionally, the margin of safety doesn’t guarantee success, and it’s important to evaluate other information such as a company’s future growth prospects, management and industry trends before making any investments decisions.

In conclusion, the margin of safety is a principle used by investors to reduce the risk of losing money when investing in stocks, bonds, or other securities by buying at a price that is below its intrinsic value. By purchasing an asset at a significant discount to its intrinsic value, investors are able to limit their potential losses and increase their chances of earning a profitable return. The margin of safety can be estimated through financial metrics and discounted cash flow models, but it’s important to note that the intrinsic value is often difficult to estimate, and it

The difference between the actual average EPS estimation and the estimation made 7 days ago

Whit this particular tool we want know if the EPS estimation of current year if is change and how much it in the last 7 Days

An earnings estimate is an analyst’s estimate for a company’s future quarterly or annual earnings per share (EPS). Future earnings estimates are arguably the most important input when attempting to value a firm. By placing estimates on the earnings of a firm for certain periods (quarterly, annually, etc.), analysts can then use cash flow analysis to approximate fair value for a company, which in turn will give a target share price.

Investors often rely on earnings estimates to analyze different stocks and decide whether to buy or sell them.

An earnings estimate is an analyst’s forecast for a public company’s future quarterly or annual earnings per share (EPS).

Investors rely heavily on earnings estimates to gauge a company’s performance and make investment decisions about it.

Most investors use a consensus earnings estimate, a forecast of a public company’s projected earnings based on the combined estimates of all equity analysts that cover the stock.

Whether a company meets, beats, or misses its earnings estimates can impact the price of the underlying stock, particularly in the short term.

Earnings surprises occur when a company misses the consensus estimate either by earning more than expected or less.

Understanding an Earnings Estimate

Analysts use forecasting models, management guidance, and fundamental information on the company to derive an EPS estimate. Market participants rely heavily on earnings estimates to gauge a company’s performance. So whether a company meets, beats, or misses its earnings estimates can impact the price of the underlying stock, particularly in the short term.

Analysts’ earnings estimates are often aggregated to create consensus estimates. These are used as a benchmark against which the company’s performance is evaluated. When you hear that a company has “missed estimates” or “beaten estimates,” it’s usually in reference to consensus estimates.

A few companies, such as Refinitiv and Zacks Investment Research, compile estimates and compute the average or consensus. Their forecasts can be found in stock quotations or financial publications such as TheWall Street Journal. Consensus numbers can also be found at a number of financial websites such as Yahoo! Finance, Bloomberg, Visible Alpha, Morningstar.com, and Google Finance.

The difference between the actual average EPS estimation and the estimation made 30 days ago

Whit this particular tool we want know if the EPS estimation of current year if is change and how much it in the last 30 Days

An earnings estimate is an analyst’s estimate for a company’s future quarterly or annual earnings per share (EPS). Future earnings estimates are arguably the most important input when attempting to value a firm. By placing estimates on the earnings of a firm for certain periods (quarterly, annually, etc.), analysts can then use cash flow analysis to approximate fair value for a company, which in turn will give a target share price.

Investors often rely on earnings estimates to analyze different stocks and decide whether to buy or sell them.

An earnings estimate is an analyst’s forecast for a public company’s future quarterly or annual earnings per share (EPS).

Investors rely heavily on earnings estimates to gauge a company’s performance and make investment decisions about it.

Most investors use a consensus earnings estimate, a forecast of a public company’s projected earnings based on the combined estimates of all equity analysts that cover the stock.

Whether a company meets, beats, or misses its earnings estimates can impact the price of the underlying stock, particularly in the short term.

Earnings surprises occur when a company misses the consensus estimate either by earning more than expected or less.

Understanding an Earnings Estimate

Analysts use forecasting models, management guidance, and fundamental information on the company to derive an EPS estimate. Market participants rely heavily on earnings estimates to gauge a company’s performance. So whether a company meets, beats, or misses its earnings estimates can impact the price of the underlying stock, particularly in the short term.

Analysts’ earnings estimates are often aggregated to create consensus estimates. These are used as a benchmark against which the company’s performance is evaluated. When you hear that a company has “missed estimates” or “beaten estimates,” it’s usually in reference to consensus estimates.

A few companies, such as Refinitiv and Zacks Investment Research, compile estimates and compute the average or consensus. Their forecasts can be found in stock quotations or financial publications such as TheWall Street Journal. Consensus numbers can also be found at a number of financial websites such as Yahoo! Finance, Bloomberg, Visible Alpha, Morningstar.com, and Google Finance.

The difference between Average EPS Estimate Current Year and EPS of Last Fiscal Year

An earnings estimate is an analyst’s estimate for a company’s future quarterly or annual earnings per share (EPS). Future earnings estimates are arguably the most important input when attempting to value a firm. By placing estimates on the earnings of a firm for certain periods (quarterly, annually, etc.), analysts can then use cash flow analysis to approximate fair value for a company, which in turn will give a target share price.

Investors often rely on earnings estimates to analyze different stocks and decide whether to buy or sell them.

An earnings estimate is an analyst’s forecast for a public company’s future quarterly or annual earnings per share (EPS).

Investors rely heavily on earnings estimates to gauge a company’s performance and make investment decisions about it.

Most investors use a consensus earnings estimate, a forecast of a public company’s projected earnings based on the combined estimates of all equity analysts that cover the stock.

Whether a company meets, beats, or misses its earnings estimates can impact the price of the underlying stock, particularly in the short term.

Earnings surprises occur when a company misses the consensus estimate either by earning more than expected or less.

Understanding an Earnings Estimate

Analysts use forecasting models, management guidance, and fundamental information on the company to derive an EPS estimate. Market participants rely heavily on earnings estimates to gauge a company’s performance. So whether a company meets, beats, or misses its earnings estimates can impact the price of the underlying stock, particularly in the short term.

Analysts’ earnings estimates are often aggregated to create consensus estimates. These are used as a benchmark against which the company’s performance is evaluated. When you hear that a company has “missed estimates” or “beaten estimates,” it’s usually in reference to consensus estimates.

A few companies, such as Refinitiv and Zacks Investment Research, compile estimates and compute the average or consensus. Their forecasts can be found in stock quotations or financial publications such as TheWall Street Journal. Consensus numbers can also be found at a number of financial websites such as Yahoo! Finance, Bloomberg, Visible Alpha, Morningstar.com, and Google Finance.

The difference between the Average EPS Estimate Current Qtr and the Last QuarterEPS

An earnings estimate is an analyst’s estimate for a company’s future quarterly or annual earnings per share (EPS). Future earnings estimates are arguably the most important input when attempting to value a firm. By placing estimates on the earnings of a firm for certain periods (quarterly, annually, etc.), analysts can then use cash flow analysis to approximate fair value for a company, which in turn will give a target share price.

Investors often rely on earnings estimates to analyze different stocks and decide whether to buy or sell them.

An earnings estimate is an analyst’s forecast for a public company’s future quarterly or annual earnings per share (EPS).

Investors rely heavily on earnings estimates to gauge a company’s performance and make investment decisions about it.

Most investors use a consensus earnings estimate, a forecast of a public company’s projected earnings based on the combined estimates of all equity analysts that cover the stock.

Whether a company meets, beats, or misses its earnings estimates can impact the price of the underlying stock, particularly in the short term.

Earnings surprises occur when a company misses the consensus estimate either by earning more than expected or less.

Understanding an Earnings Estimate

Analysts use forecasting models, management guidance, and fundamental information on the company to derive an EPS estimate. Market participants rely heavily on earnings estimates to gauge a company’s performance. So whether a company meets, beats, or misses its earnings estimates can impact the price of the underlying stock, particularly in the short term.

Analysts’ earnings estimates are often aggregated to create consensus estimates. These are used as a benchmark against which the company’s performance is evaluated. When you hear that a company has “missed estimates” or “beaten estimates,” it’s usually in reference to consensus estimates.

A few companies, such as Refinitiv and Zacks Investment Research, compile estimates and compute the average or consensus. Their forecasts can be found in stock quotations or financial publications such as TheWall Street Journal. Consensus numbers can also be found at a number of financial websites such as Yahoo! Finance, Bloomberg, Visible Alpha, Morningstar.com, and Google Finance.

The difference between the Average EPS Estimate Next Quarter and the Average EPS Estimate Current Quarter

An earnings estimate is an analyst’s estimate for a company’s future quarterly or annual earnings per share (EPS). Future earnings estimates are arguably the most important input when attempting to value a firm. By placing estimates on the earnings of a firm for certain periods (quarterly, annually, etc.), analysts can then use cash flow analysis to approximate fair value for a company, which in turn will give a target share price.

Investors often rely on earnings estimates to analyze different stocks and decide whether to buy or sell them.

An earnings estimate is an analyst’s forecast for a public company’s future quarterly or annual earnings per share (EPS).

Investors rely heavily on earnings estimates to gauge a company’s performance and make investment decisions about it.

Most investors use a consensus earnings estimate, a forecast of a public company’s projected earnings based on the combined estimates of all equity analysts that cover the stock.

Whether a company meets, beats, or misses its earnings estimates can impact the price of the underlying stock, particularly in the short term.

Earnings surprises occur when a company misses the consensus estimate either by earning more than expected or less.

Understanding an Earnings Estimate

Analysts use forecasting models, management guidance, and fundamental information on the company to derive an EPS estimate. Market participants rely heavily on earnings estimates to gauge a company’s performance. So whether a company meets, beats, or misses its earnings estimates can impact the price of the underlying stock, particularly in the short term.

Analysts’ earnings estimates are often aggregated to create consensus estimates. These are used as a benchmark against which the company’s performance is evaluated. When you hear that a company has “missed estimates” or “beaten estimates,” it’s usually in reference to consensus estimates.

A few companies, such as Refinitiv and Zacks Investment Research, compile estimates and compute the average or consensus. Their forecasts can be found in stock quotations or financial publications such as TheWall Street Journal. Consensus numbers can also be found at a number of financial websites such as Yahoo! Finance, Bloomberg, Visible Alpha, Morningstar.com, and Google Finance.

A maximum drawdown (MDD) is the maximum observed loss from a peak to a trough of a portfolio, before a new peak is attained. Maximum drawdown is an indicator of downside risk over a specified time period.

It can be used both as a stand-alone measure or as an input into other metrics such as “Return over Maximum Drawdown” and the Calmar Ratio. Maximum Drawdown is expressed in percentage terms.

Maximum drawdown is a specific measure of drawdown that looks for the greatest movement from a high point to a low point, before a new peak is achieved. However, it’s important to note that it only measures the size of the largest loss, without taking into consideration the frequency of large losses. Because it measures only the largest drawdown, MDD does not indicate how long it took an investor to recover from the loss, or if the investment even recovered at all.

Maximum drawdown (MDD) is an indicator used to assess the relative riskiness of one stock screening strategy versus another, as it focuses on capital preservation, which is a key concern for most investors. For example, two screening strategies can have the same average outperformance, tracking error, and volatility, but their maximum drawdowns compared to the benchmark can be very different.

A low maximum drawdown is preferred as this indicates that losses from investment were small. If an investment never lost a penny, the maximum drawdown would be zero. The worst possible maximum drawdown would be -100%, meaning the investment is completely worthless.

MDD should be used in the right perspective to derive the maximum benefit from it. In this regard, particular attention should be paid to the time period being considered. For instance, a hypothetical long-only U.S. fund Gamma has been in existence since 2000 and had a maximum drawdown of -30% in the period ending 2010. While this may seem like a huge loss, note that the S&P 500 had plunged more than 55% from its peak in October 2007 to its trough in March 2009. While other metrics would need to be considered to assess Gamma fund’s overall performance, from the viewpoint of MDD, it has outperformed its benchmark by a huge margin.

This risk measure shows the largest peak to trough price drop in the past 5 years. Our calculations use closing prices adjusted for dividend payments.

What Is a Maximum Drawdown (MDD)?

Drawdown in stock trading refers to the peak-to-trough decline in the value of a stock portfolio or an individual stock from its highest point to its lowest point. In other words, it’s the amount by which an investment’s value falls from its peak before a rebound or a recovery. It is a measure of risk and is an important metric for investors to track as it provides insight into the potential for future losses and the level of risk associated with a particular stock or portfolio.

There are two types of drawdown: the maximum drawdown, which is the largest peak-to-trough decline in the value of the stock or portfolio, and the drawdown duration, which is the number of days it takes for an investment to recover from its maximum drawdown to a new high.

Investors use drawdown as an indicator of risk, and a higher drawdown indicates a higher level of risk, and a lower drawdown indicates a lower level of risk. This is because a higher drawdown means that the stock or portfolio has suffered greater losses and is more susceptible to price fluctuations.

It’s important to note that a drawdown is not a measure of the overall performance of a stock or portfolio, but rather a measure of the risk associated with that stock or portfolio. A stock or portfolio that experiences a high drawdown may have a higher return over time, while a stock or portfolio that experiences a low drawdown may have a lower return over time.

In conclusion, Drawdown in stock trading refers to the peak-to-trough decline in the value of a stock portfolio or an individual stock from its highest point to its lowest point. It’s an important metric for investors to track as it provides insight into the level of risk and the potential for future losses. It’s important to note that a drawdown is not a measure of the overall performance of a stock or portfolio, but rather a measure of the risk associated with that stock or portfolio. Investors use drawdown as an indicator of risk, a higher drawdown indicates a higher level of risk, and a lower drawdown indicates a lower level of risk.

The single-quarter earnings per share announced on the last earnings report date.

PS or earnings per share is a financial metric used to measure a company’s profitability. It is calculated by dividing a company’s net income by the number of outstanding shares of stock. EPS is used to evaluate a company’s performance, particularly in comparison to its competitors and industry averages.

EPS can be estimated using a variety of methods. One of the most common is through the use of financial analysts’ estimates, which are generated by financial analysts who track the company and provide predictions for future earnings. These estimates are usually based on a combination of historical financial data and the analyst’s own assumptions about future performance.

Another method for estimating EPS is through the use of financial models such as the discounted cash flow (DCF) model, which takes into account a company’s projected future cash flows, growth rate, and discount rate. The DCF model provides a present value of future cash flows, and by subtracting the company’s present value of debt and equity, we can estimate the company’s net income and then divide it by the number of outstanding shares to estimate EPS.

It’s important to note that EPS estimates are often subject to change and may not always be accurate. Factors such as economic conditions, industry trends, and company-specific events can affect a company’s performance and may cause actual EPS to differ from estimated EPS. Additionally, it’s important to consider other financial metrics, such as revenue and return on equity, to gain a better understanding of a company’s overall performance.

In conclusion, EPS or earnings per share is a financial metric used to measure a company’s profitability. It is calculated by dividing a company’s net income by the number of outstanding shares of stock. EPS can be estimated using a variety of methods such as financial analysts estimates and financial models such as DCF. However, it’s important to note that EPS estimates are often subject to change and may not always be accurate, Factors such as economic conditions, industry trends, and company-specific events can affect a company’s performance. Additionally, it’s important to consider other financial metrics to gain a better understanding of a company’s overall performance.

The average sales estimate for the current quarter.

The average sales estimate is a financial metric used to forecast a company’s future revenue. It is typically calculated by taking the average of revenue forecasts made by a group of analysts who cover the company. These analysts may be employed by investment banks, research firms, or other financial institutions.

Average sales estimates are important for investors and traders as they provide an idea of what to expect from a company’s revenue in the future. They can be used to evaluate a company’s performance and to compare it to its peers and industry averages.

Analysts typically use a variety of methods to estimate a company’s sales, such as analyzing historical financial data, industry trends, and the company’s own guidance. They also may consider external factors such as economic conditions and competition.

It’s important to note that the average sales estimate is just that, an estimate, and actual sales figures may differ from the estimates. Additionally, analysts have varying degrees of accuracy, and the range of estimates can be wide. Therefore, investors should use average sales estimates as one of several inputs when making investment decisions and should always conduct their own due diligence.

In conclusion, the average sales estimate is a financial metric used to forecast a company’s future revenue. It’s typically calculated by taking the average of revenue forecasts made by a group of analysts who cover the company. These estimates can be used to evaluate a company’s performance and compare it to its peers and industry averages. However, it’s important to note that the average sales estimate is just an estimate and actual sales figures may differ from the estimates. Investors should use average sales estimates as one of several inputs when making investment decisions and should always conduct their own due diligence.

The average sales estimate is a financial metric used to forecast a company’s future revenue. It is typically calculated by taking the average of revenue forecasts made by a group of analysts who cover the company. These analysts may be employed by investment banks, research firms, or other financial institutions.

Average sales estimates are important for investors and traders as they provide an idea of what to expect from a company’s revenue in the future. They can be used to evaluate a company’s performance and to compare it to its peers and industry averages.

Analysts typically use a variety of methods to estimate a company’s sales, such as analyzing historical financial data, industry trends, and the company’s own guidance. They also may consider external factors such as economic conditions and competition.

It’s important to note that the average sales estimate is just that, an estimate, and actual sales figures may differ from the estimates. Additionally, analysts have varying degrees of accuracy, and the range of estimates can be wide. Therefore, investors should use average sales estimates as one of several inputs when making investment decisions and should always conduct their own due diligence.